What is Blockchain and What Can It Do for You?

Blockchain is hyped as one of the most transformative technologies to emerge in recent history. What is it, why is it important, and what problems can be solved using blockchain technologies?

Blockchain is a technology that allows for an encrypted, distributed, and public ledger. It acts as a record of transactions that is distributed among all machines participating in a network. In this way, it's owned by everyone with access to the data, and protected by cryptographic security. This cryptographic security has built-in measures to protect against hacking, or damage to the database.

Okay, so now that we know what blockchain is... Why is any of this important?

Over $270 billion worth of transactions have already taken place within this public ledger. By 2017, 15% of healthcare data was already managed by it as well. Market value of blockchain is expected to exceed $60 billion by 2020 alone. The need for law firms, contractors, banks, and other typical institutions to oversee transactions may diminish significantly, if not entirely. All transactions may become painless, no matter where in the world they are done; as well as having strong encrypted security like never before.

The dramatic entry of this technology has been characterized as follows:

"The blockchain revolution has a greater potential than anything we've seen in history. It's bigger than the Internet revolution, how it's going to restructure society." - Patrick Byrne, former CEO and founder of Overstock.com

But where does blockchain come from? How does it work, and what problems does it solve? Does it really have the potential to have a greater impact than the Internet?

In this article, we will attempt to answer these questions. We will look at the origins of blockchain, how it works in comparison to more traditional data storage tools such as relational databases, the types of problems it is used to solve, and its potential impact on the landscape of data.

Where Does Blockchain Come From?

Blockchain is best known for its role in underwriting the distributed ledger of Bitcoin. It came to be globally recognized after Bitcoin's momentous increase in value (and subsequent volatility), and as Bitcoin has gained acceptance as a legitimate digital currency. But while blockchain might be most famous because of Bitcoin, increasing attention has been paid to the many problems that distributed ledgers can help solve across a host of industries such as healthcare, finance, supply chain, and others. Examples include:

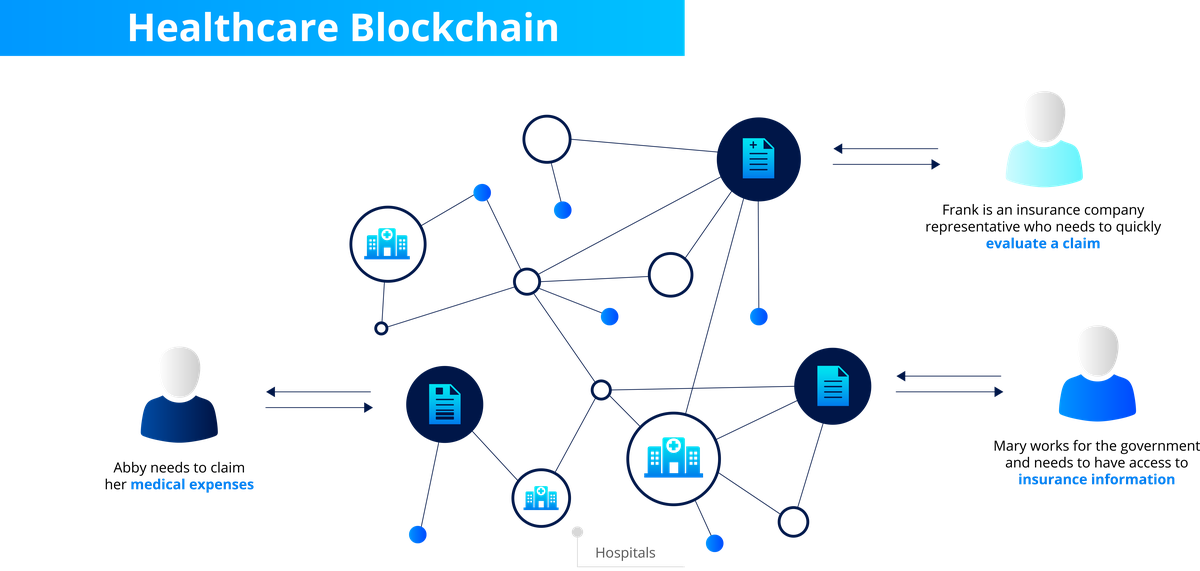

- Securing patient data. Blockchain is able to store transparent logs of patient data, and provide methods to ensure that approved individuals or organizations are able to access it.

- Payments. Moving resources across international borders has long been a major challenge. Current methods of transportation are costly, error-prone, and easily exploited. In contrast, blockchain solutions combine the best of security and transparency. Anonymous, verifiable identifiers can be used to provide transparency about the movement of funds, while still ensuring privacy and preventing abuse.

- Supply chain. Using blockchain, it is possible to assign a unique cryptographic identifier to every part or piece moving through a supply network (much in the same way that individual Bitcoins are identified). As the parts move through the network, it is possible to accurately track their progress and eventual delivery efficiently without error (often using sensor networks and other automated processes). De Beers successfully put blockchain to use to avoid the purchase of "blood diamonds" which had been mined in violent circumstances and are used to finance terrorism and conflict in Africa and other regions. Through its platform, De Beers tracks diamonds from the mine, to cutter, to polisher, and jeweler. Photos of a diamond's progress is uploaded to the blockchain alongside information about quality, color, and location. Together, the attributes create a "signature" that identifies each diamond and provides verification and helps to prevent diamonds from unknown origin entering the system.

- Helping distribute information. In particular, issues can pop up when information isn't shared with whom it needs to be. Problems can be severe if data is unreliable, or at worst, incorrect. Utilizing a blockchain system, MIT students have made it easier than ever for data to efficiently reach the medical professionals that need it most.

- Keeping asset ownership simple. With regular databases, buying or selling assets such as stocks, requires going through digital brokers, banks, and a slew of other arbiters to show ownership. Blockchain makes it far simpler, as transactions between any entities are recorded, and then represented digitally within the public ledger. This process is called "asset tokenization". This makes tracking ownership an incredibly streamlined and reliable system.

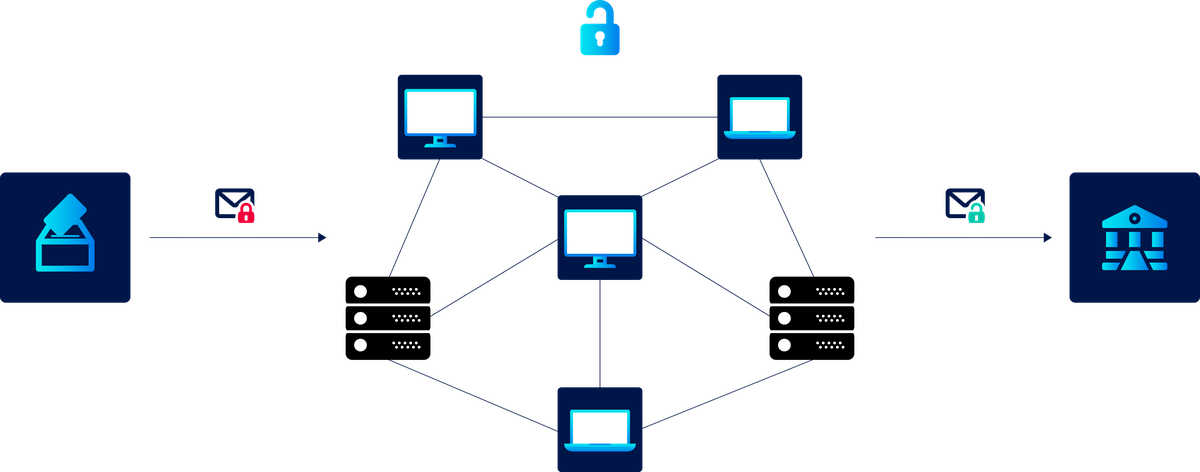

- Preventing voter fraud. Preventing voter fraud, hacking, and loss of critical data are all essential to ensuring that elections are protected. Being the most currently secure form of digital ledger, blockchain fits right in with guarding against all of these things. Blockchain's design as an encrypted, secure, and distributed database seems like the natural solution to providing a healthy democracy.

Brief History of Blockchain

Blockchain was first described in a white-paper laying out a form of digital currency. Appearing in 2009, in the midst of the Great Recession when cynicism about how governments managed money was at a high, the new currency (Bitcoin) was intended to serve as an alternative. Rather than governments controlling the finances and banking of their citizens, the paper described a technical system capable of empowering individuals to control their financial independence.

Fundamental to the way it worked was a set of technologies intended to decentralize data and its management, preventing the type of consolidation typical of more traditional storage systems (such as relational databases). This was intended to prevent governments or large corporations from controlling the future of Bitcoin.

Because of the innovative technology and idealism, Bitcoin was initially adopted by an enthusiastic community. Of interest, the author of the original paper, Satoshi Nakamoto, published the specification anonymously and still remains unidentified, adding to the drama surrounding the technology. As the implications of the data model have become clear, though, it has made further strides toward acceptance as a digital currency.

So, what makes Blockchain's treatment of data special, and how does that compare to how databases work?

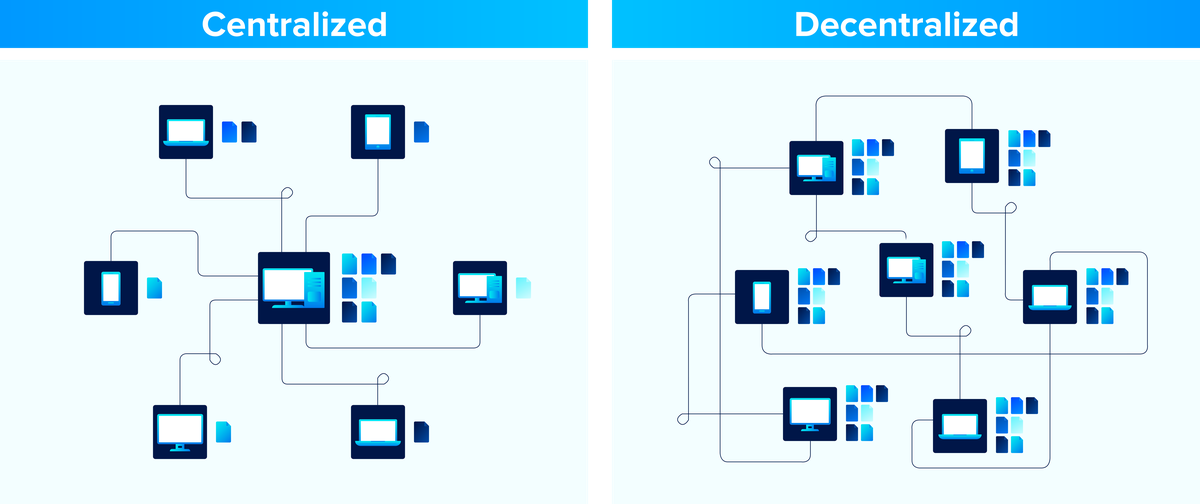

The Traditional Database

Until very recently, relational databases were considered the be-all, end-all solution to store massive amounts of data. They offer a flexible model which can be used to succinctly tabulate information and retrieve it quickly. Because of this they have been adopted by almost all major industries and serve as the backbone of data infrastructure.

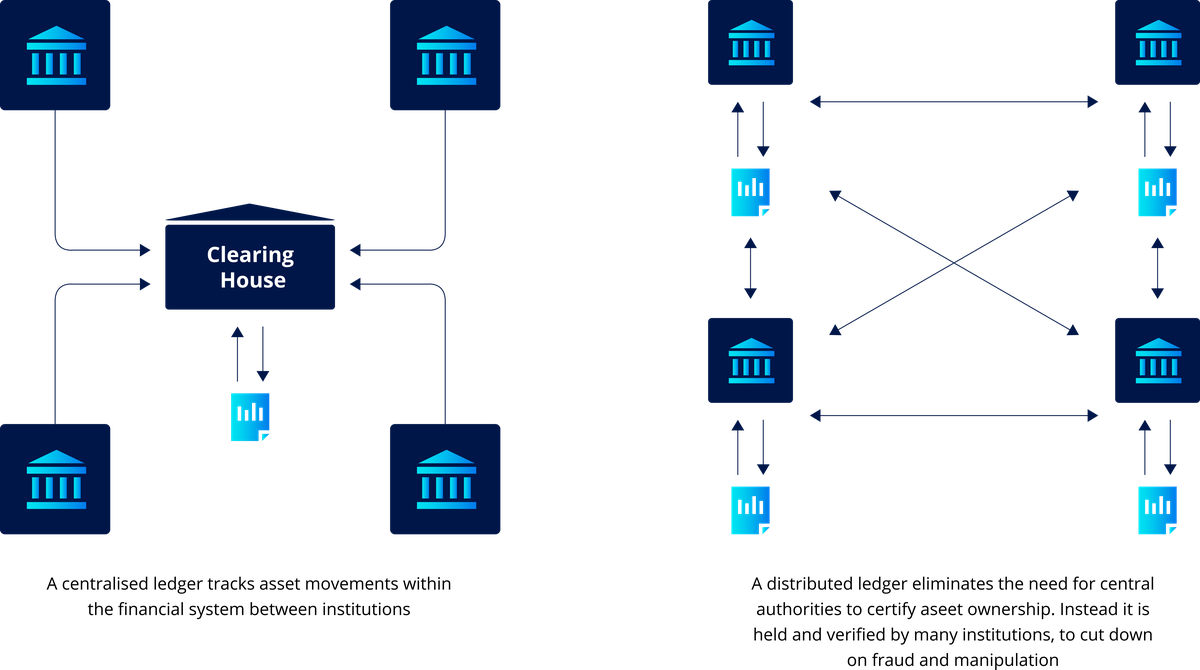

In a typical relational database, security is ensured through an administrator. Adding, removing, modifying, or retrieving data is moderated by a centralized set of of resources all controlled via the admin. Anyone needing to edit this data in any form, must also be given access to do so by the administrator.

Common Problems with Relational Databases

While this model provides a way to ensure that only trusted groups are able to access the data resources, if the admin's control over the database were to be compromised, there will be problems. Major breaches of public data such as that suffered by Equifax (which compromised the financial information of over 143 million individuals) or Home Depot (which compromised 56 million credit card numbers) have been due to the leak of database administrator credentials.

How Blockchain Works

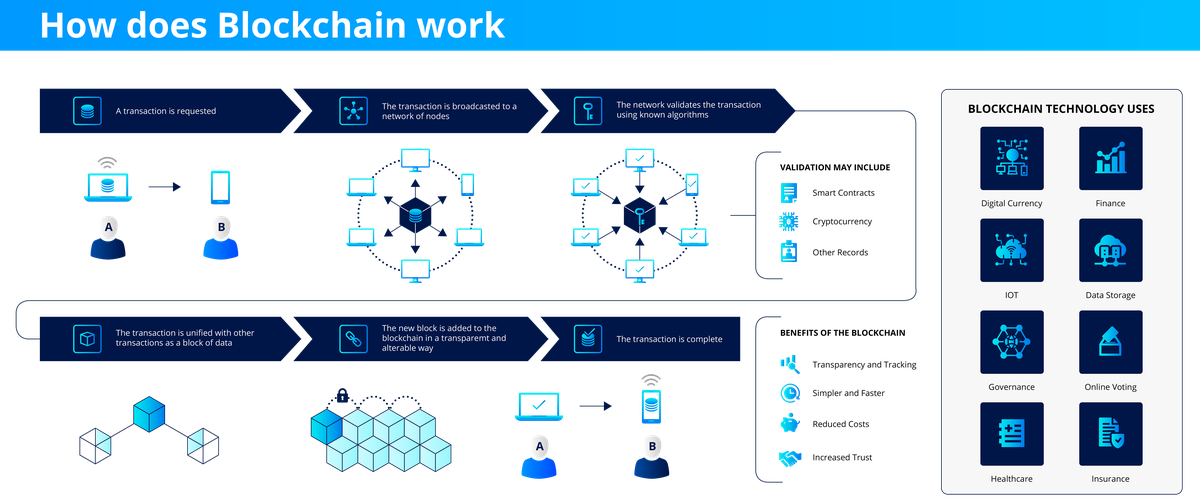

In comparison with traditional relational database design, blockchain negates many of these issues by removing a central authority entirely. Built as a decentralized ledger, every transaction is fully transparent to each node (depending on the implementation, the data might also be visible to everyone). Each transaction entry in the chain is permanent and irreversible (often called immutable) and cannot be changed by manual intervention or other nodes. Transactions are then transmitted to other nodes and signed using strong cryptographic techniques. Each time a new node comes online, a majority of the participating nodes validate the new node and sync the records of the chain.

Blockchain is a data structure where records are linked to one another as part of a log. To access later data, first you have to read earlier entries. Because of this linking and the way in which information is crytographically signed, changes have to be validated (or rejected), via consensus between the computers in the network. The specific rules for reaching consensus are decided by the chain's design. The consensus model means that individuals trying to modify or hack the chain must compromise nearly all the nodes and coordinate an update in bulk. Likewise, because new records are validated against earlier entries, attempts to change the data will be detected nearly immediately and can be reverted using the logs of other nodes to their previous values. This makes blockchain data very resilient and tamper resistant..

How Does Blockchain Compare?

Relational Database:

- Database based on one or a small set of servers, usually configured as master/slaves

- Administrators play a central role in deciding permissions and managing access to data

- Data protected using access controls, subject to centralized management

- If admin, or central authority is compromised, then the database will be as well

Blockchain (Distributed Database):

- Segments of a whole database installed on individual computers using the database

- Power shared by every computer within the network

- Changes made inside of a single node and verified by consensus. Upon validation, changes are distributed to other copies of the ledger.

- Sensitive data can be encrypted and access mediated through the use of "smart contracts", providing ways to protect information that go beyond access control mechanisms.

- Built-in security against hacking or illegal data change, with every change relying on the last

- Human error is negated, as the blockchain handles recording, and verifying data integrity. The chain is also able to restore damaged data from redundant copies of the ledger.

What Does Blockchain Solve?

Blockchains are effectively immune to hacking with the ability to both read and write data at high volume. This makes them appropriate for large data sets where transparency, immutability, security, and resiliency are important considerations. It does not mean they are the perfect tool for every challenge, though.

Some challenges of blockchain include:

- Scalability of large networks is an issue as the chain becomes large, the amount of storage required to keep a complete copy is high. Likewise, new additions to the chain might require hours to fully replicate through the entire network.

- The technology is still new, and (relatively speaking) untested. As with any emerging technologies there are a large number of implementations, and it can be difficult to agree on which platform to build applications and how to integrate against existing technology systems.

Comments

Loading

No results found